Your to-do list for becoming an attending, in the right order.

Start day one knowing nothing slipped through.

- All 32 moves, in the order to actually handle them

- Contract, disability, loans, licensing, paycheck, sequenced by when each is due

- A fillable My Transition File for your NPI, policy, and loan details

- A plain-English glossary for every term you will hit

Inside: 32 steps, sequenced across three phases

It's not just you. Nobody hands you the order.

You spent a decade learning medicine. Then in a few months you're expected to get the contract, disability, loans, and licensing right, in the right order, usually with no one you trust to ask.

I just feel completely lost and overwhelmed, and I haven't even started work yet.

I'm figuring everything out on my own, with no orientation. I've got impostor syndrome and I'm just overall miserable.

I'm about to be an attending for the first time, and I feel like I don't actually know anything. This is terrifying.

Not more to read. An order to follow.

The first decisions are the ones you can't take back.

Own-occupation disability gets more expensive, or impossible

after a single new diagnosis. The cheapest day to buy it is the first one.

A non-compete or missing tail clause can lock you in

to a job you want to leave, long after you have signed the offer.

The wrong loan move at the income jump costs tens of thousands

you never get back. Most attendings make this call out of order.

The order is done. You just work down the list.

Every move from training to practice is mapped to when you should handle it. Money and disability are folded in as steps in that order, not a separate thing to figure out later.

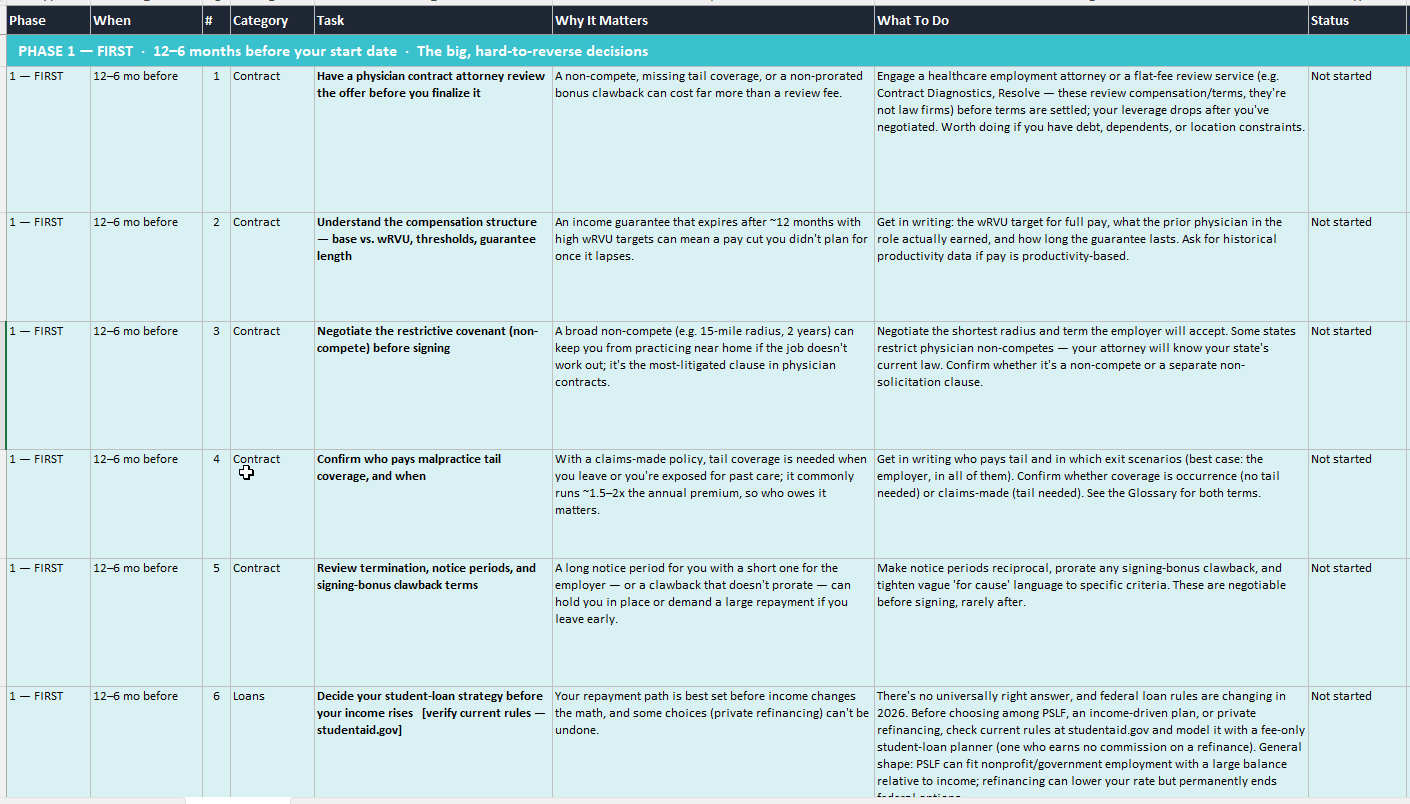

The hard-to-reverse calls

Contract review, own-occupation disability, your loan strategy, your state license.

The ones that cost the most to get wrong.

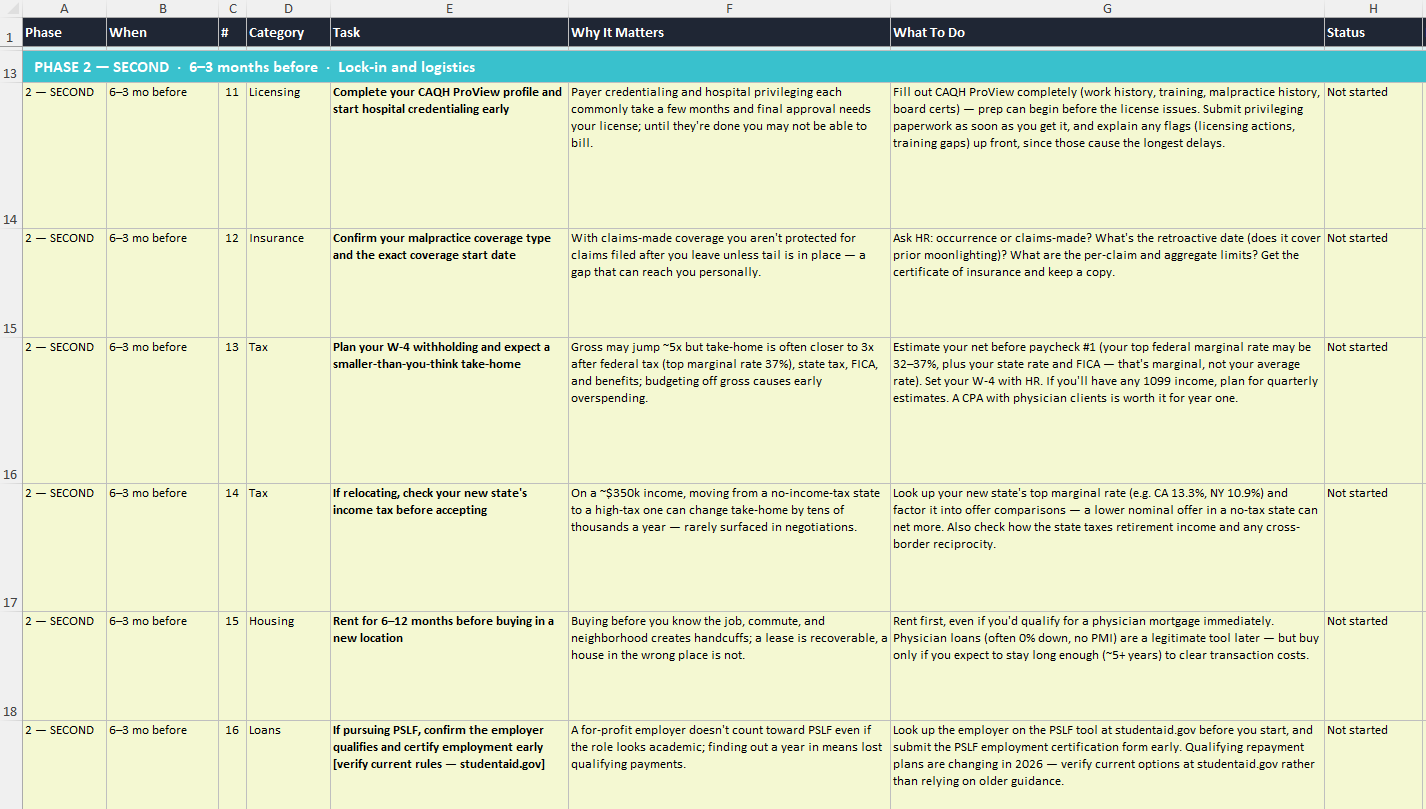

Lock-in and logistics

Credentialing and CAQH, the tax and take-home reality, rent vs. buy, PSLF vs. refinance.

The stuff that quietly delays your start date.

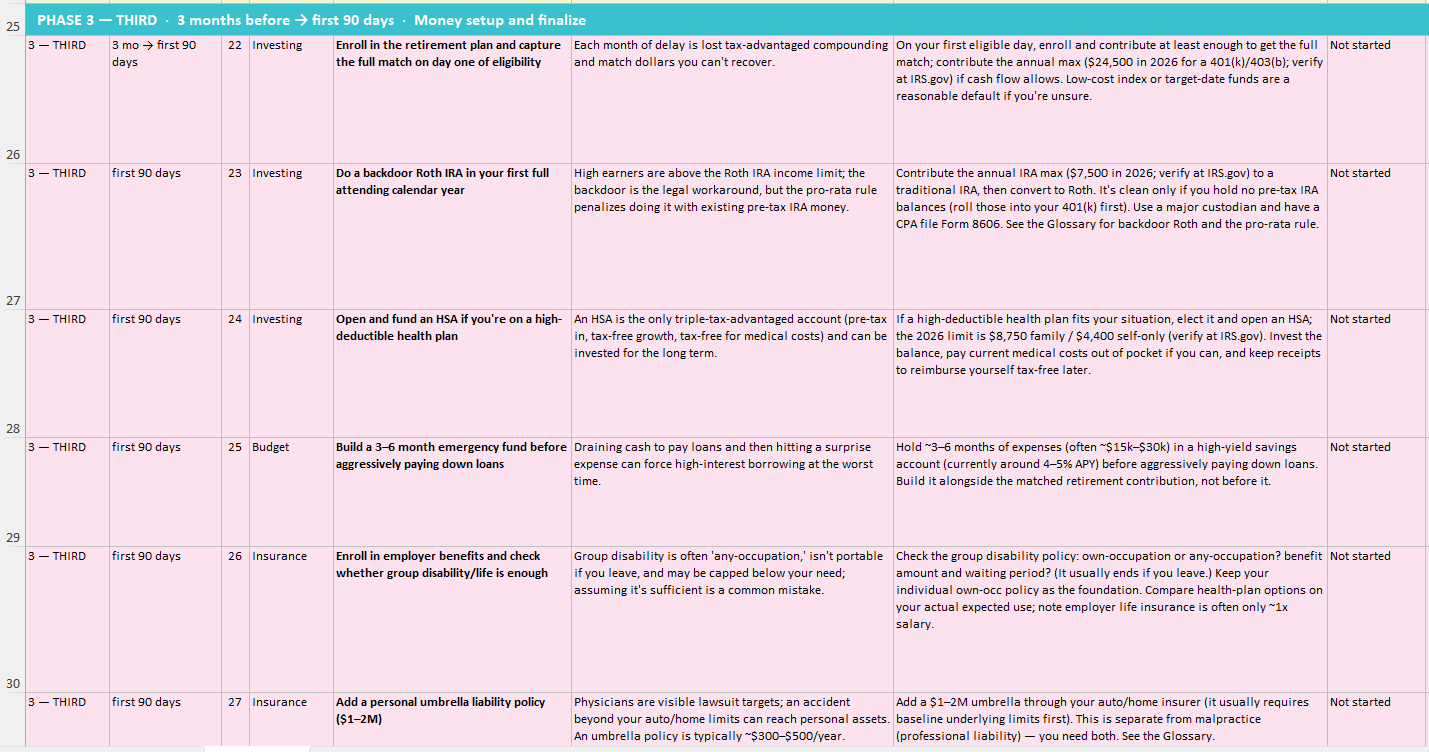

Money setup and finalize

Retirement accounts and the match, backdoor Roth, benefits, billing and your NPI.

Set these up once and stop thinking about them.

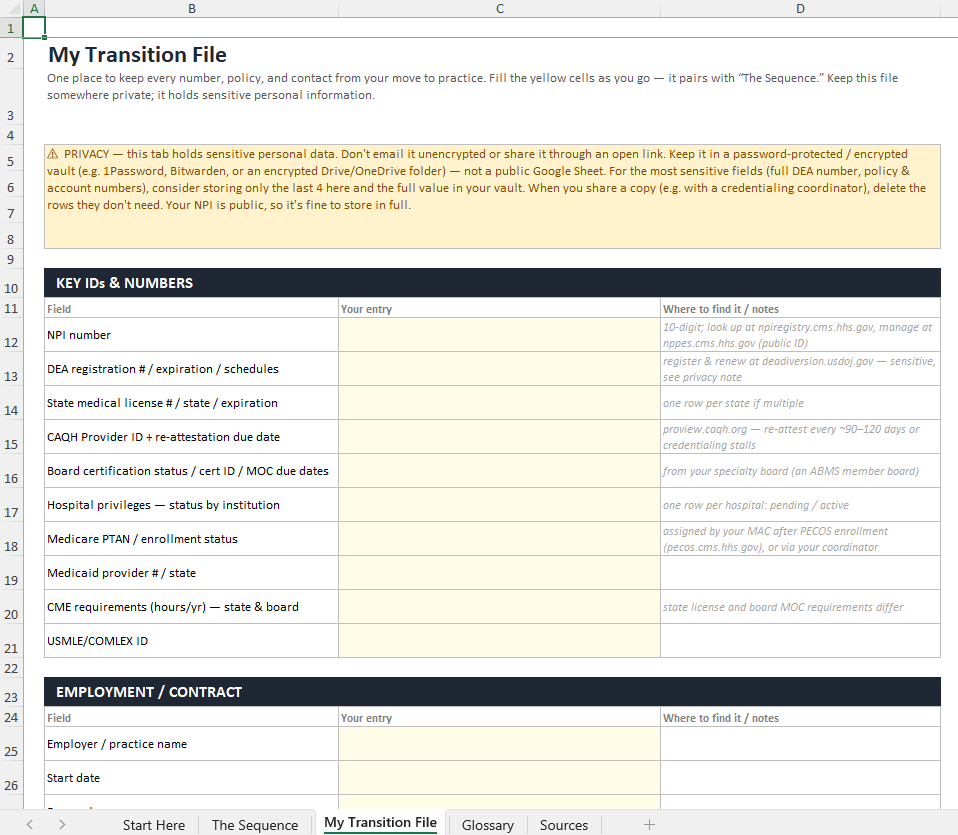

One place to store your NPI, license and DEA numbers, your disability policy, your loan plan, and the contacts you will need again.

A working spreadsheet you'll actually open.

Read it in a few minutes and judge it for yourself, before you ever talk to anyone.

The Sequence

Thirty-two steps across the three phases, with what to do and why it matters, and a box to check each off.

My Transition File

Your numbers, policies, and contacts in one place, so you stop digging through email for them.

Plain-English glossary

Own-occ, backdoor Roth, 457(b), tail coverage, PSLF. The terms, defined in a sentence each.

Built by the team that does this for physicians.

We do one thing: financial guidance built for physicians. This checklist is the same sequence we walk doctors through, so you can see exactly how we think. Yours to use first.

White Coat Investor, physician-specific advisors, and physicians talking to each other.

The tax and retirement figures are verified against the IRS, not pulled from an old blog.

It is the sequence Influent walks physicians through, not a generic checklist pulled off the internet.

The questions you are already asking.

Who is this for?

Graduating residents and fellows, and new attendings in their first year. If you are about to sign a contract or start your first job, it is built for you.

I do not have time for one more thing.

That is the reason it exists. It is a checklist you skim in a few minutes, not a course. The order is done for you.

Is the information actually accurate, and for my situation?

The steps are sourced from White Coat Investor, physician advisors, and real physician threads, with the 2026 tax numbers verified against the IRS. Where a choice depends on your situation, it tells you what to weigh so you can make the call.

Get it in order before it all lands at once.

Walk into your first attending job with the contract, disability, loans, licensing, and first paycheck already sequenced, instead of guessing at the worst possible time.

Free, and sent straight to your inbox.